All Categories

Featured

Table of Contents

This five-year general guideline and two complying with exemptions use just when the proprietor's fatality activates the payout. Annuitant-driven payouts are gone over below. The very first exemption to the general five-year policy for private recipients is to accept the fatality advantage over a longer duration, not to go beyond the expected life time of the beneficiary.

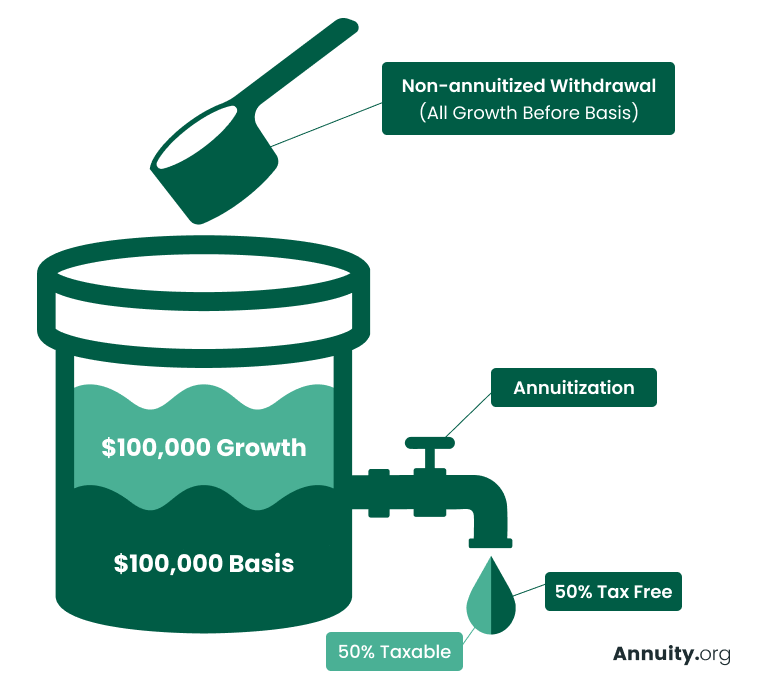

If the recipient elects to take the survivor benefit in this approach, the benefits are tired like any type of various other annuity payments: partly as tax-free return of principal and partially gross income. The exemption proportion is located by utilizing the deceased contractholder's cost basis and the expected payouts based upon the recipient's life expectations (of shorter duration, if that is what the recipient selects).

In this technique, in some cases called a "stretch annuity", the recipient takes a withdrawal yearly-- the called for amount of every year's withdrawal is based on the exact same tables utilized to determine the called for circulations from an individual retirement account. There are 2 advantages to this method. One, the account is not annuitized so the recipient preserves control over the money value in the contract.

The 2nd exemption to the five-year policy is offered just to a surviving partner. If the assigned beneficiary is the contractholder's partner, the spouse might elect to "tip into the shoes" of the decedent. In effect, the partner is dealt with as if he or she were the owner of the annuity from its inception.

Tax consequences of inheriting a Annuity Income

Please note this uses only if the partner is named as a "designated recipient"; it is not available, for example, if a trust fund is the beneficiary and the spouse is the trustee. The general five-year guideline and the two exemptions only put on owner-driven annuities, not annuitant-driven contracts. Annuitant-driven agreements will pay death benefits when the annuitant passes away.

For functions of this conversation, think that the annuitant and the proprietor are various - Annuity withdrawal options. If the agreement is annuitant-driven and the annuitant dies, the fatality activates the survivor benefit and the recipient has 60 days to determine how to take the survivor benefit subject to the regards to the annuity agreement

Note that the choice of a spouse to "step into the shoes" of the proprietor will certainly not be offered-- that exception applies only when the owner has actually passed away yet the owner didn't die in the instance, the annuitant did. Finally, if the recipient is under age 59, the "death" exemption to prevent the 10% fine will not put on a premature circulation once again, since that is readily available only on the fatality of the contractholder (not the death of the annuitant).

Several annuity firms have internal underwriting policies that refuse to release contracts that name a different proprietor and annuitant. (There may be odd circumstances in which an annuitant-driven contract fulfills a clients distinct demands, but usually the tax downsides will exceed the benefits - Variable annuities.) Jointly-owned annuities might posture similar issues-- or at least they might not offer the estate preparation function that other jointly-held properties do

Therefore, the death benefits should be paid out within 5 years of the initial proprietor's fatality, or based on the 2 exemptions (annuitization or spousal continuation). If an annuity is held jointly in between a husband and better half it would show up that if one were to pass away, the various other can simply continue ownership under the spousal continuation exemption.

Assume that the spouse and other half named their child as beneficiary of their jointly-owned annuity. Upon the fatality of either proprietor, the firm must pay the fatality advantages to the boy, who is the beneficiary, not the making it through spouse and this would probably beat the proprietor's intents. Was really hoping there may be a mechanism like setting up a recipient IRA, however looks like they is not the instance when the estate is configuration as a recipient.

That does not recognize the sort of account holding the inherited annuity. If the annuity remained in an inherited IRA annuity, you as administrator need to have the ability to assign the acquired IRA annuities out of the estate to acquired Individual retirement accounts for every estate recipient. This transfer is not a taxed occasion.

Any type of circulations made from acquired IRAs after task are taxed to the recipient that obtained them at their common earnings tax obligation price for the year of distributions. Yet if the inherited annuities were not in an IRA at her death, after that there is no method to do a direct rollover right into an inherited IRA for either the estate or the estate recipients.

If that happens, you can still pass the circulation via the estate to the individual estate recipients. The revenue tax obligation return for the estate (Type 1041) might include Form K-1, passing the revenue from the estate to the estate beneficiaries to be exhausted at their specific tax obligation prices rather than the much greater estate income tax rates.

How are Structured Annuities taxed when inherited

.jpg)

: We will certainly develop a plan that consists of the finest items and attributes, such as boosted fatality advantages, costs benefits, and long-term life insurance.: Receive a personalized strategy designed to maximize your estate's value and minimize tax obligation liabilities.: Implement the selected approach and get continuous support.: We will aid you with establishing the annuities and life insurance policy policies, offering continuous guidance to ensure the plan remains effective.

Nevertheless, ought to the inheritance be considered an income associated with a decedent, then taxes might use. Normally speaking, no. With exemption to pension (such as a 401(k), 403(b), or individual retirement account), life insurance policy earnings, and cost savings bond rate of interest, the beneficiary normally will not have to bear any type of revenue tax obligation on their acquired wide range.

The amount one can inherit from a count on without paying tax obligations depends upon various elements. The federal inheritance tax exemption (Immediate annuities) in the United States is $13.61 million for individuals and $27.2 million for couples in 2024. However, specific states may have their own estate tax guidelines. It is suggested to talk to a tax obligation specialist for accurate information on this matter.

His goal is to streamline retirement preparation and insurance, making certain that clients recognize their selections and protect the best insurance coverage at unequalled rates. Shawn is the founder of The Annuity Professional, an independent online insurance policy company servicing consumers across the USA. With this system, he and his team goal to remove the guesswork in retirement preparation by assisting individuals discover the best insurance coverage at one of the most competitive rates.

{kind=link}

Table of Contents

Latest Posts

Exploring Fixed Vs Variable Annuities A Comprehensive Guide to Investment Choices What Is the Best Retirement Option? Pros and Cons of Various Financial Options Why Fixed Indexed Annuity Vs Market-var

Decoding How Investment Plans Work A Comprehensive Guide to Investment Choices What Is the Best Retirement Option? Advantages and Disadvantages of Different Retirement Plans Why Variable Annuities Vs

Decoding Fixed Index Annuity Vs Variable Annuities Key Insights on Annuities Variable Vs Fixed Breaking Down the Basics of Pros And Cons Of Fixed Annuity And Variable Annuity Benefits of Choosing the

More

Latest Posts